July 5, 2022

One of the Ease of Doing Business Policies, sana noon pa!

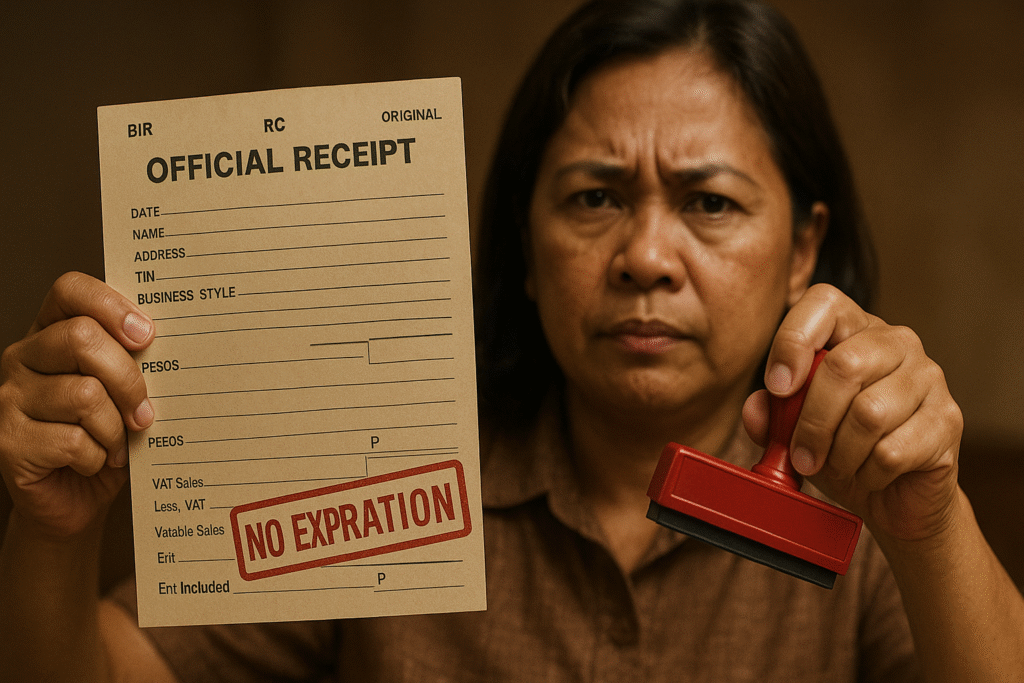

BIR Removed the Expiration of Ors/SIs!

Citing the clamor of the taxpayers in line with the Ease of Doing Business and Efficient Government Service Delivery Act of 2018, the Bureau of Internal Revenue (BIR) issued a revenue regulation mandating the removal of expiration of duly printed official receipts of a business entity or professional. One better part of this regulation is that the existing manual receipts/invoices may still be used until fully exhausted. The Authority to Print receipts/invoices inclusive of its serial numbers and its usage shall also have no more expiration, and the phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE ATP” should now be omitted and for existing unused receipts should be disregarded.

The full text of Revenue Regulation 6-2022 dated 30 June 2022 is reproduced herein:

SECTION 1. BACKGROUND

ln 2012, Revenue Regulations (RR) No. l8-2012 regulated the printing of all invoices and receipts by setting a 5-year validity period on Authority to Print (ATP). Some taxpayers clamored that they incurred additional costs in printing new sets of manual receipts/invoices once the five-year validity already lapsed despite the remaining inventory of the said receipts/invoices.

The said five-year validity was extended to the system-generated receipts/invoices issued from Cash Register Machines (CRMs), Point-of-Sale (POS) Machines and Other Sales Receipting System Software pursuant to the provisions of RR No. l0-2015, as amended. Similarly, there will be additional burden to the taxpayers if they will apply for the renewal/ reissuance of their Permit to Use (PTU) whenever the five-year validity period will transpire.

In line with Republic Act (RA) No. 11032, otherwise known as “Ease of Doing Business and Efficient Government Service Delivery Act of 2018”, the Bureau is continuously revisiting its policies and business processes to improve, streamline and reduce financial burden on the part of its clients.

SECTION 2. SCOPE

Pursuant to the provisions of Section 244 of the National Internal Revenue Code (NIRC) of 1997, as amended, these Regulations shall cover taxpayers who will apply for the following:

- ATP Official Receipts (ORs), Sales Invoices (SIs) and Other Commercial Invoices (CIs) based on Revenue Memorandum Order (RMO) No. I 2-2013;

- Registration of Computerized Accounting System (CAS)/Component of CAS based on Revenue Memorandum Circular (RMC) No. 10-2020,, RMC No. 5-2021 and RMO No. 9-2021; and

- PTU CRMs and PoS machines based on RR No. ll-2004 and RMO No. l0-2005.

SECTION 3. POLICIES AND GUIDELINES

1. The five-year validity period of the PTU and/or system-generated receipts/invoices based on the abovementioned revenue issuances is hereby removed, hence all PTUs to be issued shall be valid unless revoked by the Bureau of Internal Revenue (BIR) on grounds which shall include, but not limited to, the following:

a. Tampering of sales data/integrity of the data and/or software specification/features to alter/avoid the recording of a sale transaction;

b. Any major repair, upgrade, integration and modification/alteration without prior notification and approval by the BIR office concerned, including the items enumerated in Section V, Item No. 8 of RMO No. 9-2021, to wit:

i. Change in the functionalities of the system, particularly on enhancements that will have a direct effect on the financial aspect of the system that includes modified computations and other financial-related issues that were considered;

ii. Addition or Removal of modules or sub-modules within the system that will have a direct impact on the financial aspect of the system;

iii. Change in the system/software Version or Release Number that will have enhancements on the financial aspect of the system; and

iv. All other enhancements that will be deemed as a major system enhancement based on the recommendation of the technical evaluators of the BIR.

c. Any violation(s) on the policies and procedures for registration under RMO No. l0-2005 and RMO No. 9-2021, and other related revenue issuances.

2. The phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE PERMIT TO USE” as previously required under RR No. l0-2015 as amended by RR No.16-2018, and the phrase “Valid Until” required on RMC No. 107-2019 shall be OMITTED at the bottom portion of the system-generated receipts/invoices.

3. ATP principal and supplementary receipts/invoices inclusive of its serial numbers and its usage shall also have no expiration, thus, the phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE ATP” and the phrase “Valid Until (mm/dd/yyyy)” on the manual receipts/invoices previously required on RMO No. 12-2013 shall also be OMITTED (or DISREGARDED for unused receipts/invoices).

SECTION 4. TRANSITORY PROVISIONS

For Manual Receipts/Invoices with ATP

The validity date and the phrase as mentioned under Section 3 (3) of these regulations printed on the unused manual principal and supplementary receipts/invoices shall be disregarded and the same way may still be used until fully exhausted. Further, the subsequent printing of manual receipts/invoices upon the effectivity of these Regulations must not reflect the phrase (under Section 3 (3) of these Regulations) and shall no longer adopt the five-year validity.

For Receipts/Invoices Generated from CAS, Component of CAS with PTU or AC

All system-generated receipts/invoices that were issued with the aforementioned phrases previously required under RR No. 10-2015 as amended by RR No. I 6-2018 and RMO No. 9-2021, and RMC No. 107-2019 based on the previously approved system/software with corresponding PTU/AC shall be disregarded; however, the said system/software generating such receipts/invoices must be reconfigured to omit the said phrases.

For Receipts/Invoices Generated from CRMs and POS machines with PTU

All system-generated receipts/invoices that were issued with the aforementioned phrases previously required under RR No. 10-2015 as amended by RR No. I 6-2018, and RMC No. 107-2019, based on the previously approved CRMs and POS machines with corresponding PTU shall be disregarded; however, the said system/software generating such receipts/invoices must be reconfigured to omit the said phrases.

SECTION 5. REPEALING CLAUSE

All regulations, rules, orders or portions thereof contrary to the provisions of these Regulations are hereby repealed, amended or modified accordingly.

SECTION 6. EFFECTIVITY CLAUSE

These Regulations shall take effect fifteen (15) days after publication in the Official Gazette or in a newspaper of general circulation, whichever comes earlier.

Leave a Reply