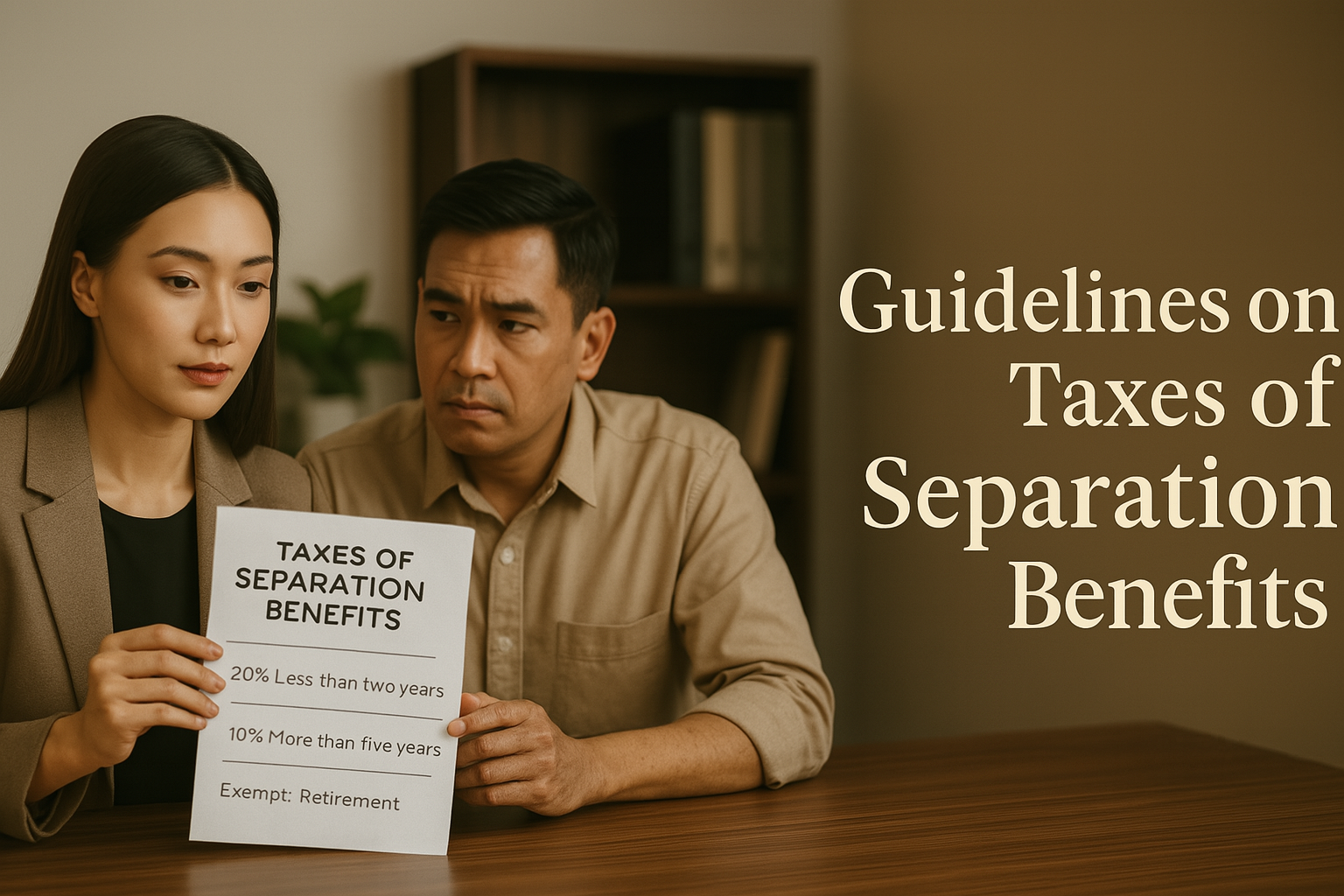

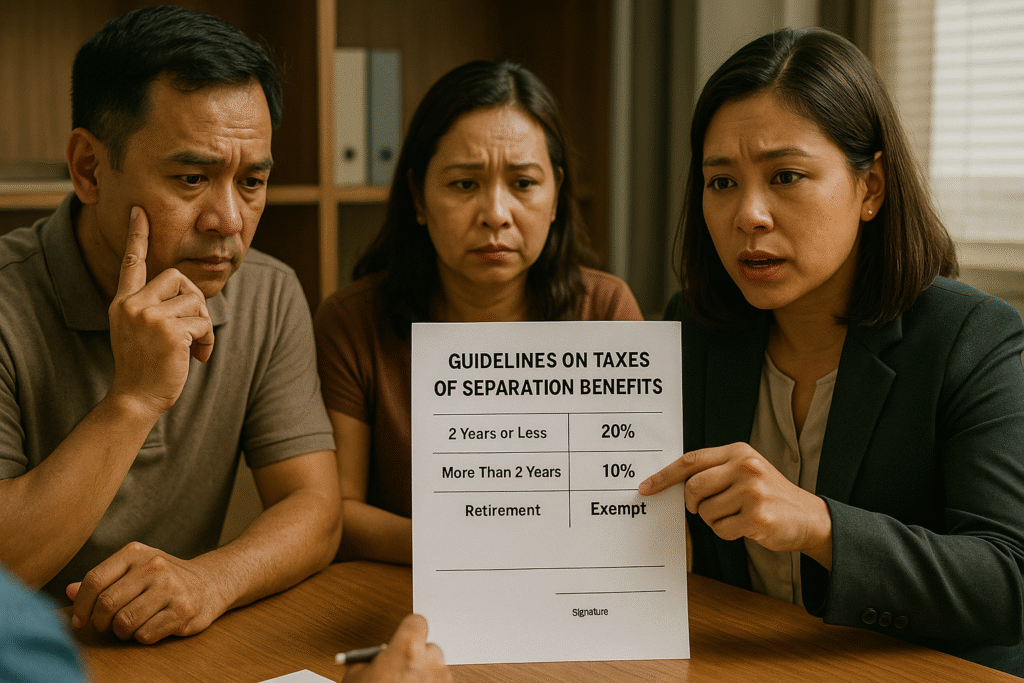

BIR Revenue Memorandum Circular Nos. 66-26 and 26-2011 provides guidelines in the tax treatment of Separation Benefits received by officials and employees on account of their separation from employment due to death, sickness or other physical disability and the issuance of Certificate of Tax Exemption from income tax and from the withholding tax.

One of the Ease of Doing Business Policies, sana noon pa!

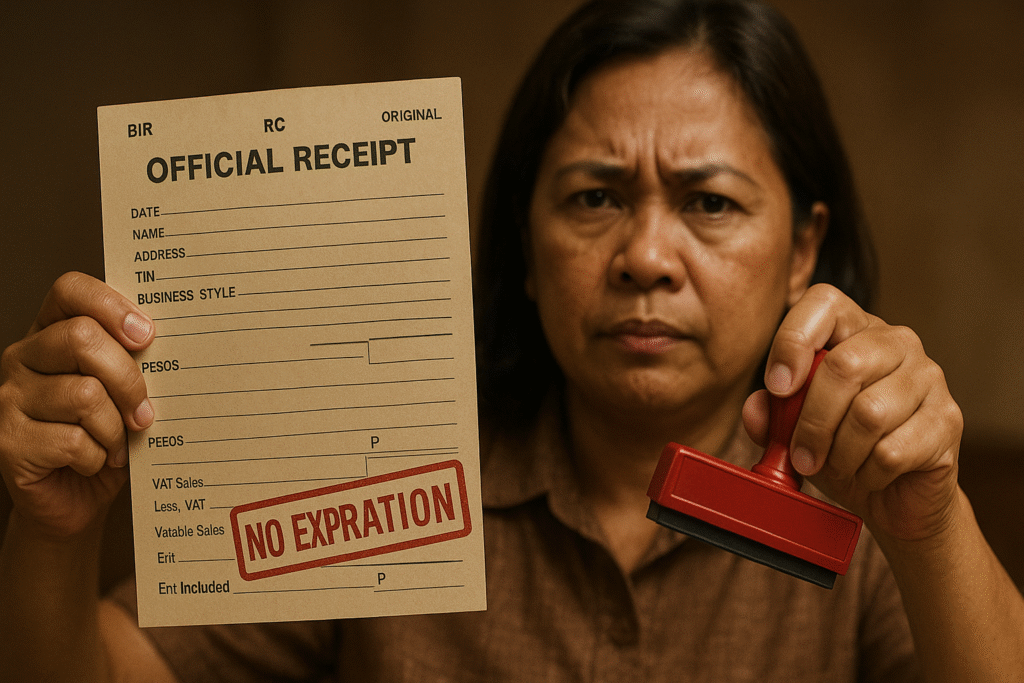

BIR Removed the Expiration of Ors/SIs!

Citing the clamor of the taxpayers in line with the Ease of Doing Business and Efficient Government Service Delivery Act of 2018, the Bureau of Internal Revenue (BIR) issued a revenue regulation mandating the removal of expiration of duly printed official receipts of a business entity or professional. One better part of this regulation is that the existing manual receipts/invoices may still be used until fully exhausted. The Authority to Print receipts/invoices inclusive of its serial numbers and its usage shall also have no more expiration, and the phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE ATP” should now be omitted and for existing unused receipts should be disregarded.

The full text of Revenue Regulation 6-2022 dated 30 June 2022 is reproduced herein:

SECTION 1. BACKGROUND

ln 2012, Revenue Regulations (RR) No. l8-2012 regulated the printing of all invoices and receipts by setting a 5-year validity period on Authority to Print (ATP). Some taxpayers clamored that they incurred additional costs in printing new sets of manual receipts/invoices once the five-year validity already lapsed despite the remaining inventory of the said receipts/invoices.

The said five-year validity was extended to the system-generated receipts/invoices issued from Cash Register Machines (CRMs), Point-of-Sale (POS) Machines and Other Sales Receipting System Software pursuant to the provisions of RR No. l0-2015, as amended. Similarly, there will be additional burden to the taxpayers if they will apply for the renewal/ reissuance of their Permit to Use (PTU) whenever the five-year validity period will transpire.

In line with Republic Act (RA) No. 11032, otherwise known as “Ease of Doing Business and Efficient Government Service Delivery Act of 2018”, the Bureau is continuously revisiting its policies and business processes to improve, streamline and reduce financial burden on the part of its clients.

SECTION 2. SCOPE

Pursuant to the provisions of Section 244 of the National Internal Revenue Code (NIRC) of 1997, as amended, these Regulations shall cover taxpayers who will apply for the following:

ATP Official Receipts (ORs), Sales Invoices (SIs) and Other Commercial Invoices (CIs) based on Revenue Memorandum Order (RMO) No. I 2-2013;

Registration of Computerized Accounting System (CAS)/Component of CAS based on Revenue Memorandum Circular (RMC) No. 10-2020,, RMC No. 5-2021 and RMO No. 9-2021; and

PTU CRMs and PoS machines based on RR No. ll-2004 and RMO No. l0-2005.

SECTION 3. POLICIES AND GUIDELINES

1. The five-year validity period of the PTU and/or system-generated receipts/invoices based on the abovementioned revenue issuances is hereby removed, hence all PTUs to be issued shall be valid unless revoked by the Bureau of Internal Revenue (BIR) on grounds which shall include, but not limited to, the following:

a. Tampering of sales data/integrity of the data and/or software specification/features to alter/avoid the recording of a sale transaction;

b. Any major repair, upgrade, integration and modification/alteration without prior notification and approval by the BIR office concerned, including the items enumerated in Section V, Item No. 8 of RMO No. 9-2021, to wit:

i. Change in the functionalities of the system, particularly on enhancements that will have a direct effect on the financial aspect of the system that includes modified computations and other financial-related issues that were considered;

ii. Addition or Removal of modules or sub-modules within the system that will have a direct impact on the financial aspect of the system;

iii. Change in the system/software Version or Release Number that will have enhancements on the financial aspect of the system; and

iv. All other enhancements that will be deemed as a major system enhancement based on the recommendation of the technical evaluators of the BIR.

c. Any violation(s) on the policies and procedures for registration under RMO No. l0-2005 and RMO No. 9-2021, and other related revenue issuances.

2. The phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE PERMIT TO USE” as previously required under RR No. l0-2015 as amended by RR No.16-2018, and the phrase “Valid Until” required on RMC No. 107-2019 shall be OMITTED at the bottom portion of the system-generated receipts/invoices.

3. ATP principal and supplementary receipts/invoices inclusive of its serial numbers and its usage shall also have no expiration, thus, the phrase “THIS INVOICE/RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF THE ATP” and the phrase “Valid Until (mm/dd/yyyy)” on the manual receipts/invoices previously required on RMO No. 12-2013 shall also be OMITTED (or DISREGARDED for unused receipts/invoices).

SECTION 4. TRANSITORY PROVISIONS

For Manual Receipts/Invoices with ATP

The validity date and the phrase as mentioned under Section 3 (3) of these regulations printed on the unused manual principal and supplementary receipts/invoices shall be disregarded and the same way may still be used until fully exhausted. Further, the subsequent printing of manual receipts/invoices upon the effectivity of these Regulations must not reflect the phrase (under Section 3 (3) of these Regulations) and shall no longer adopt the five-year validity.

For Receipts/Invoices Generated from CAS, Component of CAS with PTU or AC

All system-generated receipts/invoices that were issued with the aforementioned phrases previously required under RR No. 10-2015 as amended by RR No. I 6-2018 and RMO No. 9-2021, and RMC No. 107-2019 based on the previously approved system/software with corresponding PTU/AC shall be disregarded; however, the said system/software generating such receipts/invoices must be reconfigured to omit the said phrases.

For Receipts/Invoices Generated from CRMs and POS machines with PTU

All system-generated receipts/invoices that were issued with the aforementioned phrases previously required under RR No. 10-2015 as amended by RR No. I 6-2018, and RMC No. 107-2019, based on the previously approved CRMs and POS machines with corresponding PTU shall be disregarded; however, the said system/software generating such receipts/invoices must be reconfigured to omit the said phrases.

SECTION 5. REPEALING CLAUSE

All regulations, rules, orders or portions thereof contrary to the provisions of these Regulations are hereby repealed, amended or modified accordingly.

SECTION 6. EFFECTIVITY CLAUSE

These Regulations shall take effect fifteen (15) days after publication in the Official Gazette or in a newspaper of general circulation, whichever comes earlier.

Full digitalization of the Bureau of Internal Revenue will be a huge game changer.

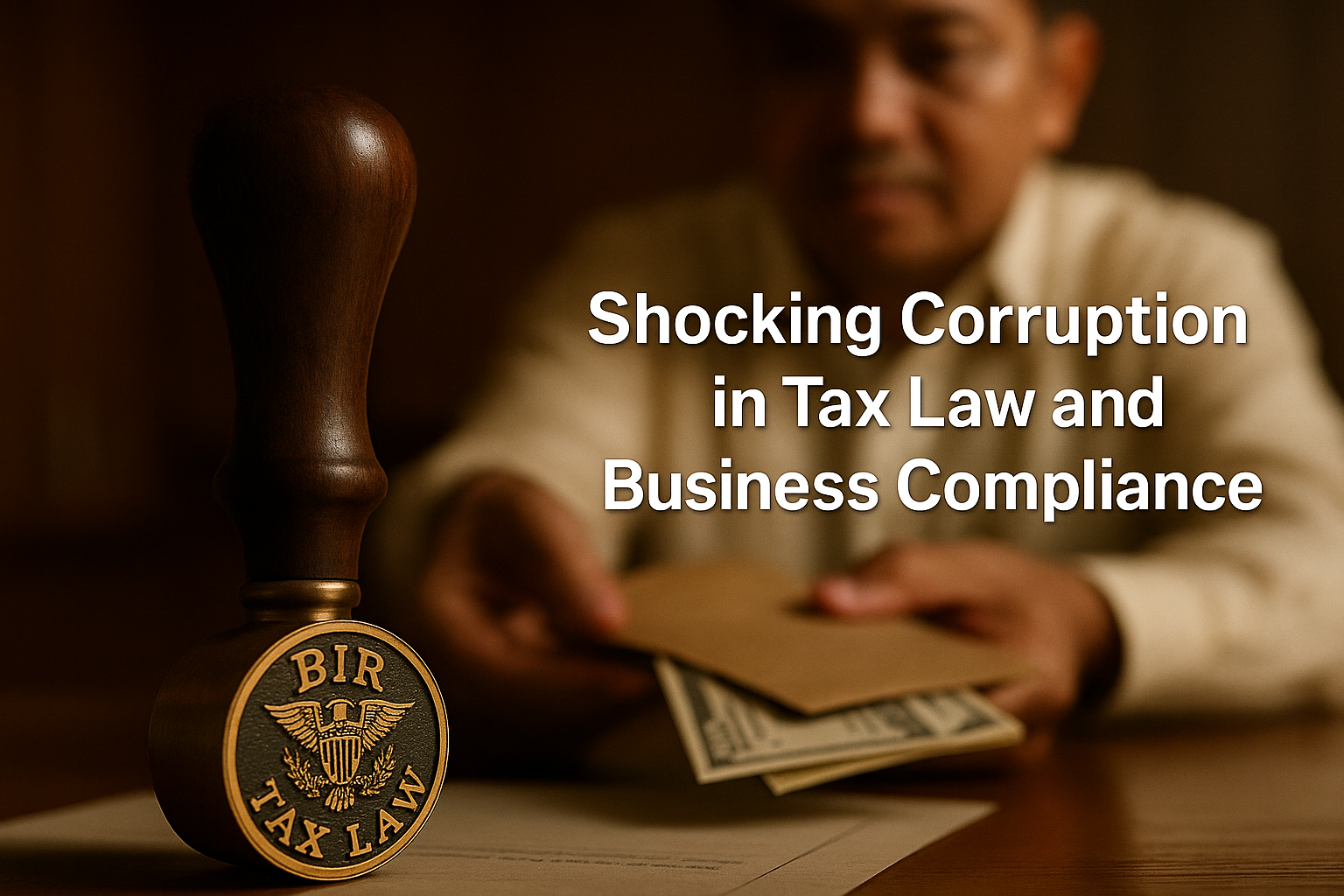

My colleague related to me her recent experiences in transacting with the Bureau of Internal Revenue (BIR). That experience gave her a nightmare she could not even imagine. Unfortunately, that is not an uncommon experience of persons dealing with the BIR. How would you feel if you are assured that a BIR personnel will assist you when you transact with them? Anybody could only imagine the feeling of exhilaration once introduced to a BIR personnel who promised to help and lessen tax liabilities arising from a simple transaction of buying and selling a piece of land. Of course, anyone will be glad. But the nightmare will get into one’s nerves once he/she is informed that such person (the BIR personnel) will rake inscrutable and gigantic amount of money from the transaction. Such BIR personnel’s share is larger than what the government will receive. The funny thing is that they can always devise means to lower the taxes payable but they must get half of the amount they insist was saved by the taxpayer. Take note that they always find ways to lower the liability in such a gargantuan difference. It is no wonder if from time to time you hear news about a BIR personnel being entrapped by NBI agents.

For example, in a purchase of a parcel of land for the amount of 100 million pesos, the taxpayer must pay capital gains tax or VAT and documentary stamp tax in the amount of, let’s say, 30 million pesos. These BIR magicians will offer a computation of taxes which is way lower than the usual, let’s say, 6 million pesos, and using the computations of BIR magicians, the taxpayer will only pay a lowered tax of 6 million. However, to be able to enjoy such a lowered computation, the taxpayer must agree to give to the BIR personnel half of the 24 million which is the amount supposedly saved by the taxpayer. In effect, the taxpayer, in concert with the BIR magicians, would be able to save 12 million pesos and actually deceive the government the amount of 24 million pesos. Who will not be tempted to bite this? But that will never be shared to a taxpayer until the taxpayer agrees to settle the tax liability in a manner they showed it. Because the taxpayer always wants to pay a lower amount of tax, he/she will always agree to the proposal.

In another example, when a Letter of Authority (LOA) from the BIR is issued to a business entity, the end result would almost always be settlement without opening the books of accounts of such company. A LOA empowers a revenue officer of the BIR to examine the books of accounts and other accounting records of a taxpayer to enable the BIR to assess and collect the correct amount of taxes. The LOA will be followed by a preliminary assessment for a huge amount. The BIR examiner would always find errors and lapses in the taxpayer’s books. Penalties and surcharges will always be imposed. Unfortunately, in-house accountants and business owners would always be willing to settle so that their books may not be opened. Sometimes, even the companies or business owners who are most ready to present their books would end up settling.

In this instance corruption comes in during settlement. There would be negotiation and tax liability may be lowered for a price. Sometimes, a 20 million pesos tax liability could be lowered to as low as 1 million pesos provided the company taxpayer agrees to give a certain amount which is almost always higher than 1 million pesos, the amount which will be paid to the government. In the end, the taxpayer wins, the examiner wins but the government loses.

The above stories are just examples of events that further degrade the integrity of the BIR and be labelled as one of the most corrupt agencies of the government. Every Filipino prays that this trend will change. Unfortunately, this practice seemed to be embedded already in such agency’s bureaucratic practices. As long as the BIR personnel or assessor or collector or officer has discretion in determining how much is the tax liability of a taxpayer, all transactions in that agency are prone to being tainted with corruption.

One of the solutions, I believe, is to remove the discretion from the BIR personnel. For example, in the collection Authorizing of taxes arising from the sale of real property, the process of securing the Certificate Registration (CAR) should be in such a way that the taxpayer and the BIR personnel could not negotiate. I am happy to hear a statement of the new BIR commissioner saying, “I am committed to strengthening tax administration through digitalization. This will make the tax collection system more efficient and less prone to graft and corruption.”[1] Digitalization will certainly lessen corruption in a colossal degree. Digitalization should be programmed in such a way that the taxpayer would have no choice but to pay the correct taxes. The discretion of the BIR examiner or assessor must be removed. In securing a CAR for transfer of titles of real properties for example, the BIR system[2] must automatically compute the tax liability once data are entered. There must also be a devise to ensure that the taxpayers and/or the BIR personnel are entering the correct data in every transaction. It should just be a mere PASS/FAIL or COMPLIED/UNCOMPLIED type of system totally removing the discretion of any BIR personnel. It must be completely automated and devoid of any human intervention. I still couldn’t imagine what type of computer system or program is needed to lessen, if not totally eradicate, the corruption in that agency. But with the many transactions I had with that agency, I strongly believe that digitalization will certainly make a difference.